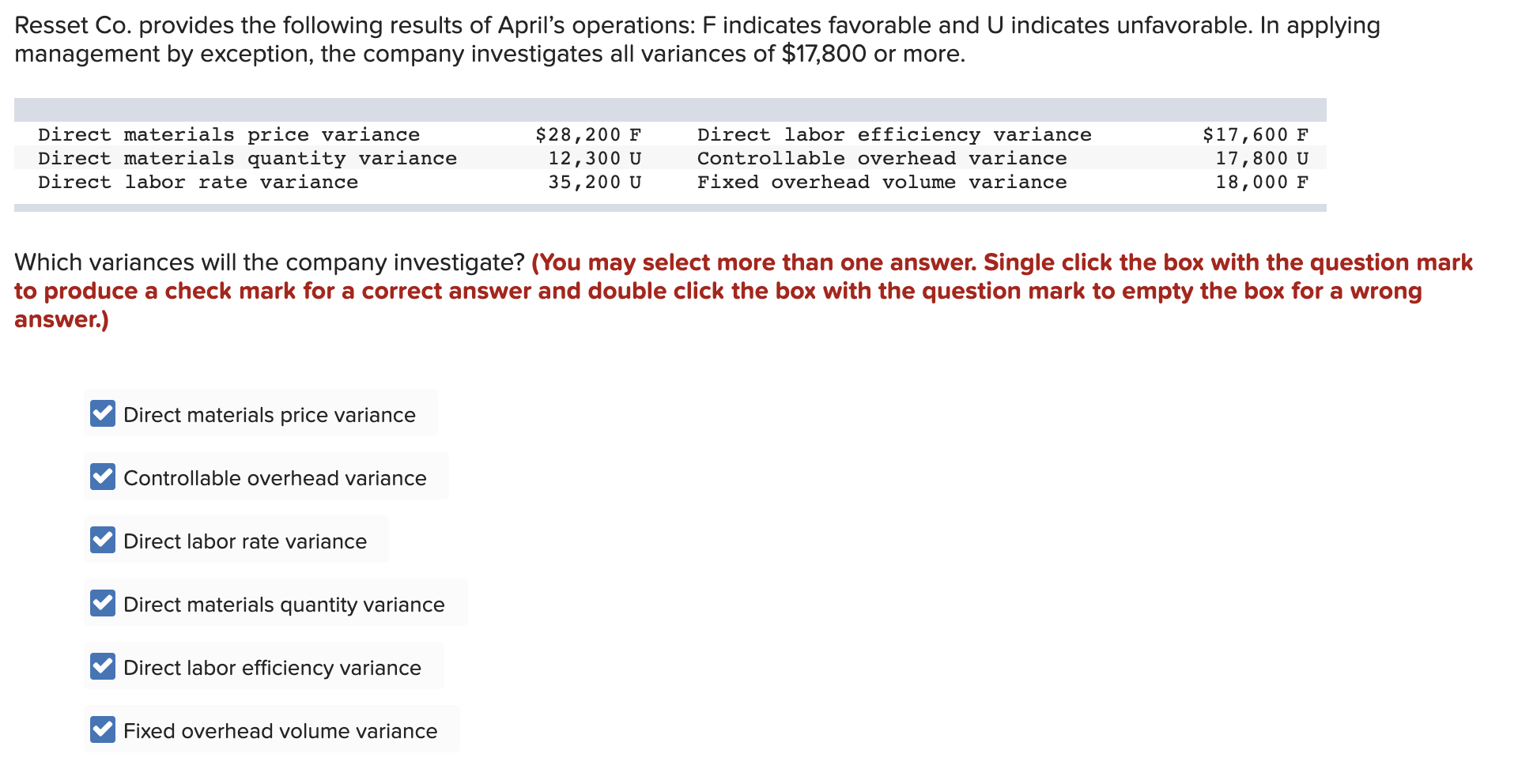

During planning, you come up with a standard or budgeted price of $5 per pound for aluminum. When you review your actual costs, you find that the real price paid was $5.75 per pound. Unfavorable efficiency variance means that the actual labor hours are higher than expected for a certain amount of a unit’s production. If we compute for the actual rate per hour used (which will be useful for further analysis later), we would get $8.25; i.e. $325,875 divided by 39,500 hours. It is crucial as it flags discrepancies between planned and actual labor hours, pinpointing inefficiencies.

Rate Variance and Efficiency Variance

An employer’s overhead cost per employee is also considered, in addition to the employer’s annual taxes. If the total actual cost is higher than the total standard cost, the variance is unfavorable since the company paid more than what it expected to pay. Labor rate variance arises when labor is paid at a rate that differs from the standard wage rate. Labor efficiency variance arises when the actual hours worked vary from standard, resulting in a higher or lower standard time recorded for a given output. One of the best ways to monitor labor efficiency is, for sure, using time-tracking software.

- All tasks do not require equally skilled workers; some tasks are more complicated and require more experienced workers than others.

- The actual hours worked are the actual number of hours worked to create one unit of product.

- Some of the workers in a factory perform tasks that are directly linked to the manufacturing process.

- Addressing these challenges requires a comprehensive approach involving continuous evaluation, industry foresight, and a nuanced understanding of the production landscape.

Types of Labor Cost Variance

This variance assessment offers critical insights into operational efficiency and resource allocation within a business framework. If customer orders for a product are not enough to keep the workers busy, the production managers will have to either build up excessive inventories or accept an unfavorable labor efficiency variance. The first option is not in line with just in time (JIT) principle which focuses on minimizing all types of inventories. Excessive inventories, particularly those that are still in process, are considered evil as they generally cause additional storage cost, high defect rates and spoil workers’ efficiency.

Direct Labor Mix Variance

If anything, they try to produce a favorable variance by seeing more patients in a quicker time frame to maximize their compensation potential. If the outcome is unfavorable, the actual costs related to labor were more than the expected (standard) costs. If the outcome is favorable, the actual costs related to labor are less than the expected (standard) costs. From the payroll records of Boulevard Blanks, we find that line workers (production employees) put in 2,325 hours to make 1,620 bodies, and we see that the total cost of direct labor was $46,500. Based on the time standard of 1.5 hours of labor per body, we expected labor hours to be 2,430 (1,620 bodies x 1.5 hours). At first glance, the responsibility of any unfavorable direct labor efficiency variance lies with the production supervisors and/or foremen because they are generally the persons in charge of using direct labor force.

The Formula for Direct Labor Mix Variance

Due to these reasons, managers need to be cautious in using this variance, particularly when the workers’ team is fixed in short run. In such situations, a better idea may be to dispense with direct labor efficiency variance – at least for the sake of workers’ motivation at factory floor. Labor Efficiency Variance (LEV) is a key metric in managerial accounting that helps in evaluating the efficiency of labor used during a production process. It compares the actual hours worked to the standard hours that should have been worked to produce a certain amount of output, valued at the standard labor rate. If the exam takes longer than expected, the doctor is not compensated for that extra time. Doctors know the standard and try to schedule accordingly so a variance does not exist.

Managerial Accounting

The units produced are the equivalent units of production for the labor cost being analyzed. Labor efficiency variance is also known as labor time variance and labor usage variance. Labor price variance equals the standard hourly rate you pay direct labor employees minus the actual hourly rate you pay them, times the actual hours they work during a certain period. For example, assume your small business budgets a standard labor rate of $20 per hour and pays your employees an actual rate of $18 per hour. In this case, the actual rate per hour is $7.50, the standard rate per hour is $8.00, and the actual hour worked is 0.10 hours per box.

A labor rate variance is a measure between the total amount paid for labor and the standard amount paid. Labor rate variance is the total difference between the total paid amount for a certain amount of labor and the standard amount that the labor usually commands. Managers can better address this situation if they have a breakdown of the variances between quantity and rate. The standard hours allowed figure is determined by multiplying direct labor hours established or predetermined to produce a single unit by the number of units produced. For example, if standard time to produce one unit of a product is 2 hours and 10 units of product have been manufactured during the period than the standard time allows would be 20 hours (2 × 10).

This data prompts a focused investigation into production bottlenecks, enabling corrective action. Addressing these discrepancies enhances resource utilization, productivity, and cost control, which is vital for optimizing operations and ensuring the efficient use of labor within a business or manufacturing setting. The Labor Efficiency Variance (LEV) measures the difference between expected and actual labor hours, highlighting areas where productivity falls short. Its purpose is to identify inefficiencies, aiding in targeted improvements within the production process for better resource utilization. Monitoring labor hours is as important as comparing them to the standard hours allowed.

Connie’s Candy paid $1.50 per hour more for labor than expected and used 0.10 hours more than expected to make one box of candy. The same calculation is shown as follows using the outcomes of the direct labor rate and time variances. The total direct labor variance is also found by combining the direct labor rate variance and the direct labor time variance. child tax credit schedule 8812 By showing the total direct labor variance as the sum of the two components, management can better analyze the two variances and enhance decision-making. The combination of the unfavorable direct labor efficiency variance of $4,000 + the unfavorable direct labor rate variance of $5,520 is the total unfavorable direct labor variance of $9,520.